Rupee vs Dollar —

How Exchange Rates

Move Steel Prices

A comprehensive explanation of how the rupee vs dollar exchange rate influences the iron and steel industry in India — from raw material costs and import prices to domestic mill pricing and what it means for contractors, fabricators, and steel traders across the country.

Currency moves daily. For current mill-linked steel prices in Raipur, contact us directly.

Send EnquiryFill the contact form Join WhatsApp ChannelDaily rate updatesThe rupee vs dollar exchange rate is one of the most important — and most misunderstood — forces shaping steel prices in India. When the rupee weakens, imported coking coal, scrap, and finished steel all cost more in rupee terms. When it strengthens, import prices ease and domestic mills face competitive pressure. This guide explains the full chain of how rupee vs dollar movements travel from the currency market to the steel price you pay at your local stockist — and what you as a buyer, fabricator, or contractor can do with that information. All analysis in this article is general and educational in nature; it does not constitute financial or market advice.

- Why the Rupee vs Dollar Rate Matters for Steel — Import dependency, dollar-denominated commodities

- Raw Materials Priced in Dollars — Coking coal, iron ore, scrap, ferroalloys

- Imports, Exports & Competitive Dynamics — How currency changes trade economics

- How Exchange Rate Reaches the Steel Price — From currency market to your stockist

- Weak Rupee vs Strong Rupee — Full Impact Comparison

- Other Factors That Drive Steel Prices — Currency is not the only driver

- What This Means for Contractors & Fabricators

- Procurement Guidance in a Volatile Currency Market

- FAQ — Rupee vs Dollar & Steel Prices

Why the Rupee vs Dollar Rate Matters for Steel

India's Steel Industry • Import Dependency • Dollar-Denominated Commodities

India is one of the world's largest steel producers — yet its iron and steel industry remains deeply connected to global commodity markets priced in US dollars. Even steel produced entirely within India depends on inputs — primarily coking coal — that are sourced internationally and priced in USD. This is why the rupee vs dollar exchange rate is one of the most closely watched indicators by steel mills, traders, and large buyers across the country.

Fig 1 — Rupee vs Dollar (INR/USD) — the exchange rate that connects global commodity markets to India's domestic steel price.

India's Position in Global Steel

India's steel industry has grown significantly over the past two decades and is now among the world's largest in terms of crude steel output. Despite this scale, the industry remains a significant importer of key inputs — particularly coking coal from Australia, the USA, Canada, and Russia — all priced in US dollars. Refer to the World Steel Association for current verified production and trade statistics.

When the rupee vs dollar rate moves, the rupee cost of importing these materials changes — even if the dollar price of the commodity itself has not changed. This creates a direct cost pressure on Indian steel mills that is entirely separate from global commodity price movements.

The Dollar-Rupee Connection in Simple Terms

The mechanism can be illustrated with a simplified, hypothetical example (figures are illustrative only and do not represent any specific market prices):

If a tonne of coking coal costs USD 200 and the exchange rate is ₹80 per dollar, the rupee cost is ₹16,000 per tonne.

If the rupee weakens to ₹85 per dollar — with the dollar coal price unchanged — the same tonne now costs ₹17,000. That is a ₹1,000 per tonne increase driven entirely by rupee vs dollar movement — not by any change in the global coal market.

This additional cost eventually flows through the mill's cost of production and, in time, to the price of steel at the domestic level.

All price figures, exchange rates, and percentage estimates in this article are illustrative examples only. They do not represent current market data, historical prices, or any form of market prediction or financial advice. Steel prices and currency rates change continuously. Always consult your supplier and qualified financial advisors before making significant procurement or business decisions based on currency or commodity expectations.

Raw Materials Priced in Dollars — The Steel Input Chain

Coking Coal • Iron Ore • Steel Scrap • Ferroalloys • Ocean Freight

To understand the full impact of rupee vs dollar on steel prices, it helps to map the major raw material inputs and their currency exposure. The more dollar-denominated a mill's input basket, the more directly its production costs are affected by exchange rate movements.

Fig 2 — Steel's dollar-denominated inputs: coking coal, iron ore, and scrap are all traded globally in USD — making the rupee vs dollar rate a direct cost variable for Indian steelmakers.

Coking Coal — The Most Dollar-Sensitive Input

Coking coal (metallurgical coal) is the most critical dollar-priced input for India's blast furnace-based integrated steel plants. India imports the large majority of its coking coal requirement, primarily from Australia. Every rupee of depreciation against the dollar increases the rupee cost of this coal — directly inflating the cost of pig iron and finished steel from integrated producers.

Electric arc furnace (EAF) steel producers, who use scrap rather than coal, are somewhat less exposed to coking coal dollar risk — but steel scrap is also largely traded in dollar-denominated international markets, maintaining their currency exposure through a different input.

Iron Ore, Scrap & Other Inputs

Iron ore is available domestically in India, reducing — but not eliminating — dollar exposure. However, international iron ore benchmark prices (referencing Australian and Brazilian ore) still influence domestic ore pricing and the import parity reference.

Steel scrap for EAF producers is partly domestic but significant imported volumes — from the Middle East, Europe, and the USA — are priced in dollars. Ferroalloys and ocean freight are also USD-denominated, creating a multi-channel currency exposure for Indian steelmakers. All of these compound simultaneously when the rupee vs dollar rate shifts.

| Raw Material | Pricing Currency | India Import Dependence | Rupee vs Dollar Sensitivity |

|---|---|---|---|

| Coking Coal | USD (international benchmarks) | Very high — majority imported | High |

| Iron Ore | Domestic pricing + USD influence | Mostly domestic — some imports | Moderate |

| Steel Scrap | USD for imported scrap | Significant for EAF producers | Moderate–High |

| Ferroalloys | USD-linked international benchmarks | Partial imports | Moderate |

| Ocean Freight | USD | All imported cargo | High |

| LNG / Natural Gas | Partially USD-linked | Partial LNG imports | Partial |

How Rupee vs Dollar Movements Affect Steel Imports & Exports

Import Competitiveness • Export Advantage • Domestic Price Floor

Currency movements affect not just input costs — they also change the competitive dynamics between imported and domestically produced steel, and between selling in India versus exporting. The rupee vs dollar rate plays a direct role in both import substitution and export competitiveness for India's steel sector.

🟩 When the Rupee Weakens (Higher INR/USD)

- Imported steel becomes more expensive in rupee terms — reducing the attractiveness of imports relative to domestic supply

- Domestic mills get protection from cheaper import competition — can support domestic price levels

- Indian steel exports may become more competitive in global markets — the same rupee revenue translates to fewer dollars, making Indian steel appear cheaper to foreign buyers

- Export-oriented mills may benefit from increased foreign demand as India becomes a more competitive source

- Input costs (coking coal, scrap, freight) rise in rupee terms — compressing margins unless domestic prices rise proportionally

🟨 When the Rupee Strengthens (Lower INR/USD)

- Imported steel becomes cheaper in rupee terms — increasing competitive pressure on domestic mills from imports

- Domestic mills may face downward price pressure as import parity falls and buyers gain import alternatives

- Indian steel exports may become less competitive globally — the same dollar revenue now translates to more rupees, effectively pricing Indian steel higher for foreign buyers

- Input costs ease in rupee terms — mills see raw material cost relief if domestic price levels hold steady

- Buyers of imported finished goods or steel products benefit from lower rupee costs for dollar-priced material

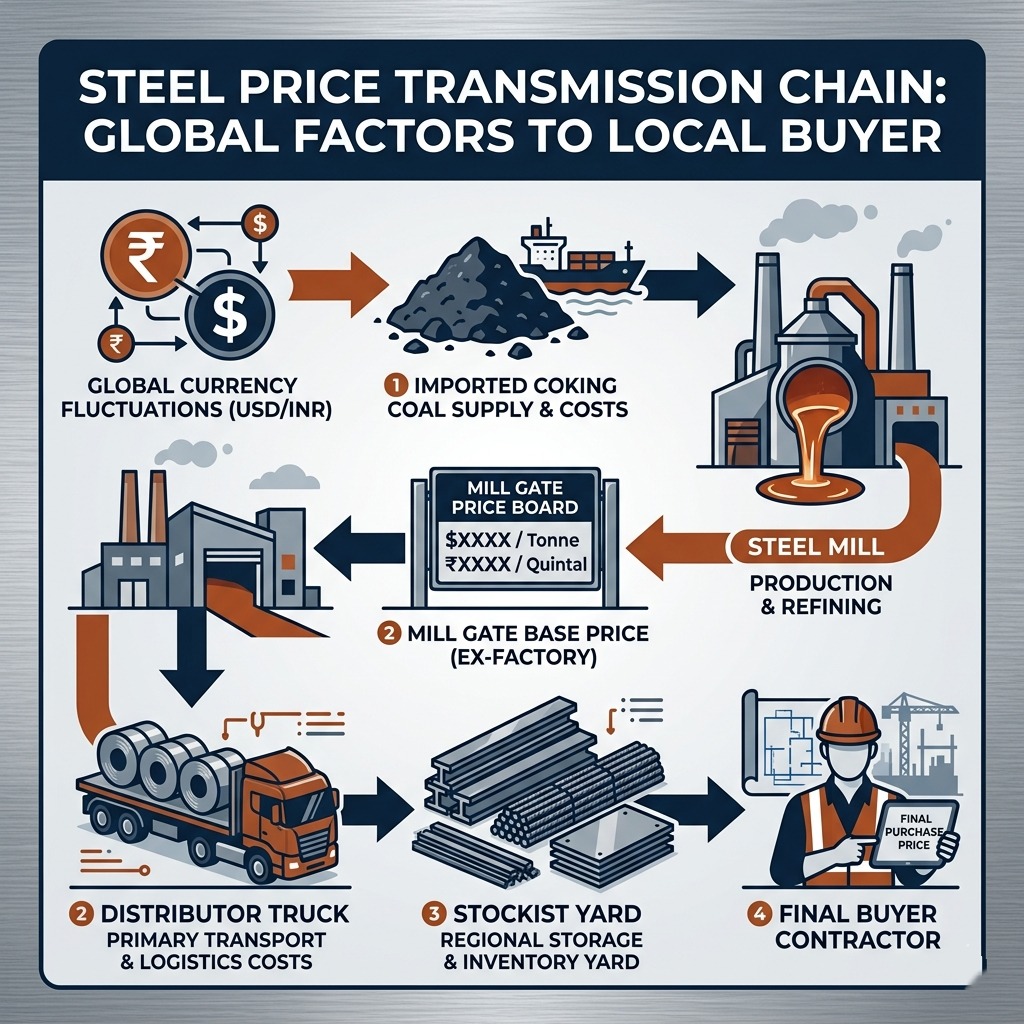

How Exchange Rate Reaches the Steel Price at Your Stockist

Currency Market → Mill Cost → Mill Price → Distributor → Stockist → Buyer

Currency movement does not instantly appear in the price of TMT bars, MS angles, or I beams at your local steel yard. There is a transmission chain with meaningful time lags, competing forces, and decision points at each stage. Understanding this chain helps buyers and fabricators interpret currency news more calmly — and avoid over-reacting to short-term exchange rate headlines.

Fig 3 — The steel price transmission chain: currency market moves → raw material cost → mill production cost → mill-gate price → distributor → stockist → end buyer. Each link adds time lag and its own pricing considerations.

Step 2: Rupee cost of imported raw materials rises

Step 3: Mill production cost increases (with a time lag)

Step 4: Mill revises its declared base price (mill-gate revision)

Step 5: Distributor / C&F agent adjusts landed cost accordingly

Step 6: Stockist reprices new incoming stock

Step 7: End buyer — contractor / fabricator — sees revised price

Why the Time Lag Exists

Steel mills do not reprice their output every time the currency fluctuates. Most large Indian steel producers revise prices on a periodic basis — often monthly, sometimes more frequently during volatile periods. Between formal revisions, prices remain stable even if the rupee vs dollar rate has moved.

Additionally, mills and distributors carry inventory purchased at earlier raw material costs. Pricing existing inventory may not fully reflect the latest currency movement — until the next purchase cycle begins and the full cost is absorbed.

When the Currency Effect Is Strongest

The rupee vs dollar effect on steel prices is most visible when the currency move is large, sustained over multiple weeks, and coincides with global commodity price movement in the same direction. Short, sharp fluctuations that quickly reverse are often absorbed within existing margins.

The effect is also stronger when domestic demand is firm — giving mills the ability to pass through cost increases — and weaker when demand is soft, forcing mills to absorb costs rather than raise prices. This is why tracking currency alone gives an incomplete picture of steel price direction.

Weak Rupee vs Strong Rupee — Full Steel Industry Impact

Two Scenarios • Winners & Losers • What to Watch Across the Value Chain

The rupee vs dollar rate creates a complex web of effects across the steel value chain — and the same currency move can benefit some participants while hurting others simultaneously. Here is a structured breakdown of both scenarios.

Weak Rupee — Integrated Steel Mills

Higher rupee cost for imported coking coal squeezes margins — unless domestic prices rise to compensate. Mills with significant export revenue have a partial natural hedge — dollar export earnings convert to more rupees, partly offsetting higher input costs. The net effect on any specific mill depends on its export-to-domestic sales ratio and the hedging strategy it employs.

Weak Rupee — Traders & Stockists

Existing inventory purchased at pre-depreciation costs may show an apparent windfall as prices rise. However, replenishing that inventory at new higher costs erodes future margins unless selling prices track the input cost increase. Traders holding large stock at old prices during a sharp rupee move face both opportunity and risk simultaneously.

Weak Rupee — Contractors & Fabricators

For fabricators and contractors, the weak rupee is a pure cost risk. They have no dollar revenue to offset the increase. The greatest exposure is for businesses with fixed-price project contracts that were quoted before the currency move — where steel costs may rise mid-project with no ability to recover the increase from the client.

Strong Rupee — Full Value Chain

A stronger rupee eases input costs for mills, lowers import parity prices, and increases competitive pressure from cheaper imports. End buyers — contractors, fabricators, and project developers — generally benefit from more competitive steel pricing. Export-oriented mills may see reduced export competitiveness. The overall domestic steel market may experience more subdued pricing during periods of sustained rupee strength.

It is tempting to conclude that a weaker rupee always means higher steel prices — but this is an oversimplification. A weaker rupee coinciding with weak global steel demand, falling international coal prices, or government import duty reductions can produce a very different outcome. Steel prices respond to the simultaneous interaction of many forces. The rupee vs dollar rate is one important input into this system — not the only one, and not always the dominant one. Always assess the full market context rather than drawing procurement conclusions from currency movements in isolation.

Other Factors That Drive Steel Prices — Beyond Rupee vs Dollar

Global Demand • Government Policy • Energy Costs • Domestic Supply & Inventory

Focusing only on the rupee vs dollar rate gives an incomplete picture of what moves steel prices. Here are the other major forces that interact with — and sometimes override — the currency effect in determining what you pay for structural steel at your stockist.

Global Steel Demand

China accounts for a significant share of global steel production and consumption. Any meaningful shift in Chinese domestic demand or export behaviour ripples through global steel prices — affecting the reference benchmarks Indian mills use to set domestic prices, regardless of where the rupee vs dollar stands.

Government Policy & Duties

India has used import duties, minimum import prices, and anti-dumping measures to regulate steel imports. These policy tools can quickly insulate or expose domestic steel prices from global movements — including currency-driven ones. Policy changes can shift competitive dynamics rapidly and are often difficult to anticipate.

Energy Costs

Electricity, natural gas, and fuel are major cost components for steel production — particularly for EAF producers. Rising energy costs can increase domestic steel production costs independently of any currency movement, adding a further layer to the pricing equation that is separate from the rupee vs dollar effect.

Domestic Demand Cycle

Construction activity, infrastructure spending, and manufacturing growth drive domestic steel demand. Strong domestic demand gives mills the pricing power to pass through cost increases. Weak demand forces mills to absorb increases rather than raise prices — meaning the same currency move can produce very different price outcomes in different demand environments.

Coking Coal & Ore Spot Prices

Even with a stable rupee vs dollar rate, a sharp rise in international coking coal prices inflates production costs directly. The currency and commodity price effects compound each other — when both coking coal prices and the dollar rise together against the rupee, the cost impact on Indian mills is particularly large.

Inventory & Market Sentiment

Mills and traders carry inventory purchased at prior cost levels, acting as a short-term price buffer. When industry inventory is high, mills may delay price increases even as costs rise. When inventory is tight, price revisions move faster. Tracking inventory sentiment through your supplier network is a practical early indicator of near-term price direction.

Fig 5 — Steel prices respond to a combination of forces simultaneously: the rupee vs dollar rate is one of several — domestic demand, global commodity prices, energy costs, and government policy all interact with currency to produce the final price.

What Rupee vs Dollar Movement Means for Contractors & Fabricators

Project Cost Risk • Fixed-Price Contracts • Material Planning

For contractors, fabricators, and building materials buyers, the rupee vs dollar rate is a background risk that occasionally becomes acutely visible — typically when a large, sustained currency move coincides with a steel mill price revision. Here is how currency-driven price changes flow through to real project outcomes.

Fixed-Price Contracts — The Highest Risk Zone

If you have quoted a fixed price to your client for a project with significant structural steel content — and the rupee weakens materially before you have purchased all your steel — you face a margin squeeze that has nothing to do with your own efficiency or planning.

This is the most common way that rupee vs dollar volatility creates real financial pain for construction professionals. A project priced at steel rate ₹X per kg in January can become loss-making by March if currency-driven price revisions push steel to ₹X + 12% — and many Indian building contracts do not include material price escalation provisions.

Discussing material price escalation clauses with clients before signing contracts is a practical, widely accepted risk management approach — especially on projects with long execution timelines or high steel intensity. Seek legal and commercial advice on the appropriate clause structure for your specific situation.

Inventory Timing — Risks of Trying to Predict

Some larger buyers attempt to time their steel purchases around currency and price expectations — purchasing ahead of an anticipated rise or deferring in anticipation of a fall. While this can sometimes work, it carries real risks that are often underestimated:

• Currency and commodity markets are genuinely difficult to predict — even for professional traders

• Holding excess inventory has financing, storage, insurance, and quality-management costs

• A price expected to rise may fall if market conditions change unexpectedly

• Early purchases strain cash flow and working capital

• Over-ordering ties up funds that may be needed for project execution

For most small and medium fabricators, a requirement-driven procurement approach — buying to confirmed project needs with a short lead buffer — is more appropriate than attempting to speculate on currency-driven price movements. Consult a qualified advisor before making large speculative purchases.

You do not need to track currency markets daily to benefit from basic awareness. When news reports that the rupee has weakened meaningfully against the dollar over several consecutive weeks — typically 3–5% or more — it is a reasonable prompt to contact your steel supplier and ask about upcoming price revision plans. This gives you access to confirmed information on which to base your purchasing decisions — rather than reacting to speculation or rumour.

Procurement Guidance in a Volatile Rupee vs Dollar Environment

Practical Steps • Supplier Communication • Risk Awareness • Not Financial Advice

You cannot control the rupee vs dollar rate — but you can manage your exposure to it through better procurement practices, stronger supplier relationships, and smarter project planning. The guidance below is general and educational. It does not constitute financial, legal, or commercial advice — consult qualified professionals for significant business decisions.

Stay Informed Without Over-Reacting

Track the rupee vs dollar rate as a background business indicator — not as a daily trading signal. Reliable, free sources include the Reserve Bank of India (RBI) website for the official reference rate, and major financial news outlets for weekly summaries. Vishwageeta Ispat's WhatsApp channel also provides regular rate and price update notifications — a practical way for steel buyers to stay connected to market movements without spending significant time on market research.

The key insight: not every currency move leads to a steel price change. Use currency awareness as a prompt to ask your supplier — not as an automatic trigger to purchase or defer.

• Review INR/USD rate as a weekly background indicator

• Contact your supplier when the rupee moves significantly (e.g. 2–3%+ over a short period) to ask about upcoming price revisions

• Confirm mill prices before placing large orders — get it in writing

• For long-duration projects, discuss material escalation provisions with your client and legal advisor

• Maintain relationships with at least two steel suppliers for competitive comparison

Build Awareness into Project Pricing

For larger projects or longer execution timelines, consider including a material price contingency buffer in your project cost estimate — separate from general project contingency. The appropriate buffer size depends on the steel intensity of the project, the time between quotation and execution, and your assessment of current market volatility at the time of quoting.

For smaller projects with short timelines — typically 2–4 weeks between quoting and purchasing — a confirmed price from your steel supplier at the time of quotation usually provides adequate certainty. The risk of a large, sustained price move in such a short window is generally limited, though not absent.

The guidance in this section is general and educational only. It does not constitute financial, legal, accounting, or business advice. For significant procurement contracts, material escalation clause structure, or large financial commitments influenced by currency expectations — always engage a qualified chartered accountant, financial advisor, or legal professional. Vishwageeta Ispat does not provide financial advisory services.

• Reserve Bank of India (RBI) — Official INR/USD reference rates and currency policy

• Ministry of Steel, Government of India — Steel industry data, trade statistics, and policy updates

• World Steel Association — Global steel production data, trade statistics, and industry analysis

Rupee vs Dollar & Steel Prices — Most Asked Questions

FAQ • For Contractors, Fabricators & Steel Buyers

Vishwageeta Ispat — Raipur, Chhattisgarh

Vishwageeta Ispat is Raipur's trusted iron and steel stockist — supplying TMT bars, MS angles (IS 808), ISMB I beams, ISMC channels, MS round pipes (IS 1239), square MS pipes (IS 4923), GI pipes, MS sheets, chequered plates, and all structural steel products. In a market where rupee vs dollar movements can shift prices quickly and without notice, we ensure our customers always have access to confirmed, current pricing — so you can plan and purchase with confidence.

Need today's steel rates? Our team provides mill-linked, competitive pricing on all steel sections and products. Join our WhatsApp channel for daily updates, or contact us directly for project-specific quotes — we respond the same working day.